Summary

- McKesson's share price has reacted negatively on news of Amazon's entry into the pharmacy space. I see this reaction as being unwarranted.

- Meanwhile, McKesson continues to show operating strength, and the tentative opioid litigation settlement removes an overhang.

- I find the shares to be undervalued, based on my valuation model.

The healthcare sector was rocked by the news on Nov. 17th, that Amazon Pharmacy (AMZN) will allow customers in the U.S. to order prescription medications for home delivery, including free delivery for Amazon Prime members. McKesson (MCK) was not immune to negativity from the investment community. Since the close of trading on Nov. 16th, McKesson's share price has dropped by 8%, to $169.03 as of writing. I believe this negativity is overblown, and in this article, I show what makes McKesson an attractive buy at the current valuation, so let's get started.

(Source: Company website)

A Look Into McKesson

McKesson is a 187-year-old healthcare company based in Irving, Texas, and is the biggest of the 'Big 3' pharmaceutical distributors. Perhaps one overlooked fact is that it is ranked #8 on the Fortune 500 list due to its massive revenues and reach. McKesson is a leader in healthcare supply chain management, retail pharmacy, healthcare technology, community oncology and specialty care. In FY 2020, McKesson generated $231 billion in revenue.

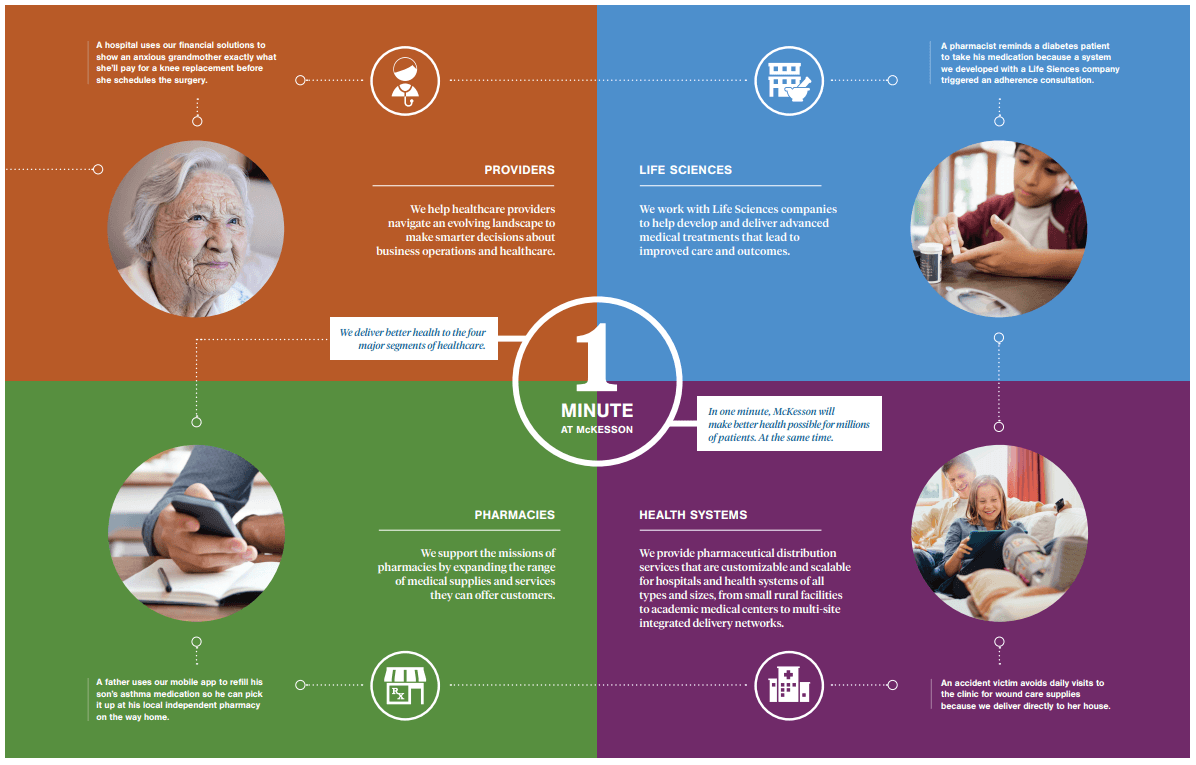

Its 80,000 employees enable McKesson reach one-third of all US pharmacies and a significant number of health systems. McKesson also has 275,000+ SKUs of branded and private label medical surgical supplies. If you have family or friends who work in hospital, it's likely that they interact with McKesson products on a daily basis. As seen below, McKesson serves as a critical link between healthcare providers, pharmacies, health systems, and life sciences.

(Source: Company website)

As mentioned earlier, I see the share price drop on the news of Amazon's entry into the pharmaceutical space as being unwarranted, and it appears to be a knee-jerk reaction. That's because Amazon's move was largely anticipated, since it acquired PillPack in 2018 for $750M+, and so this move shouldn't come as a surprise.

In addition, while McKesson does have a retail pharmacy practice in health systems, this is not its core business. In addition, its retail pharmacies in health systems serve an essential role in patient advisory and monitoring, as it is often the first stop for patients upon discharge. This is supported by the following note on McKesson's website:

Health system retail pharmacies have the opportunity to interact with more patients at discharge and between visits, including follow-up and long-term monitoring of their care, medication adherence and progress. This interaction is especially critical in high-risk transplant, cancer, HIV, cardiac or diabetes patients-and it matters to hospitals' documentation efforts, providing continuity of care and helping reduce readmissions."

Plus, McKesson's core business revolves around pharmaceutical and medical supplies distribution (with over 275K branded and private label SKUs), to pharmacies and healthcare systems. As such, Amazon could actually be a customer of McKesson in sourcing its prescription medications. Goldman Sachs (GS) appears to agree that the share price drop presents a "buy the dip" opportunity, as it recently added McKesson to its Conviction Buy List. It also doesn't view Amazon's pharmacy business as being a significant threat, as noted below (quoted from Seeking Alpha summary):