Summary

- Indiscriminate selling in the energy sector has brought the once fairly valued names like PSX to being materially undervalued.

- PSX has a network of refining and midstream assets that are near impossible to replace. Environmental regulations make it practically impossible to replicate the assets PSX has.

- In addition, its refining segment will benefit going forward because of all the refinery capacity rationalization that's happening right now (higher cost refineries permanently shutting down).

- PSX also has a great track record of returning capital back to shareholders. It has reduced shares outstanding by ~33% since 2012 all the while paying out $26 billion in dividends total.

- At trough cycle multiple of 11x FCF and a sustainable dividend yield of ~7%, we see PSX as a great buy at today's price.

- This idea was discussed in more depth with members of my private investing community, HFI Research. Get started today »

Welcome to the idea edition of Oil Markets Daily!

"Low prices cure low prices."

That's an investment adage that's attributed to commodity/cyclical businesses, and this applies to refineries as well. Because of COVID-19 and the forced shutdown initiated by governments worldwide, refineries have been hit especially hard. This makes sense since oil demand is reflected via the end-consumer demand of products, and if no one is using it, then product storages build and push refining margins down.

A good illustration of this is the US refining margin tracker used by Energy Aspects:

Source: EA

Now, similar to the crude futures curve, the curve is not to be used as a predictor of future oil prices, but rather the current fundamentals projected out forward without assuming any material changes. So, if oil demand recovers or product storages start to draw, then these refining margins will move up as a result.

And in order for oil prices to start sustainably move higher, global refining margins will have to improve OR global refining capacity would have to be reduced.

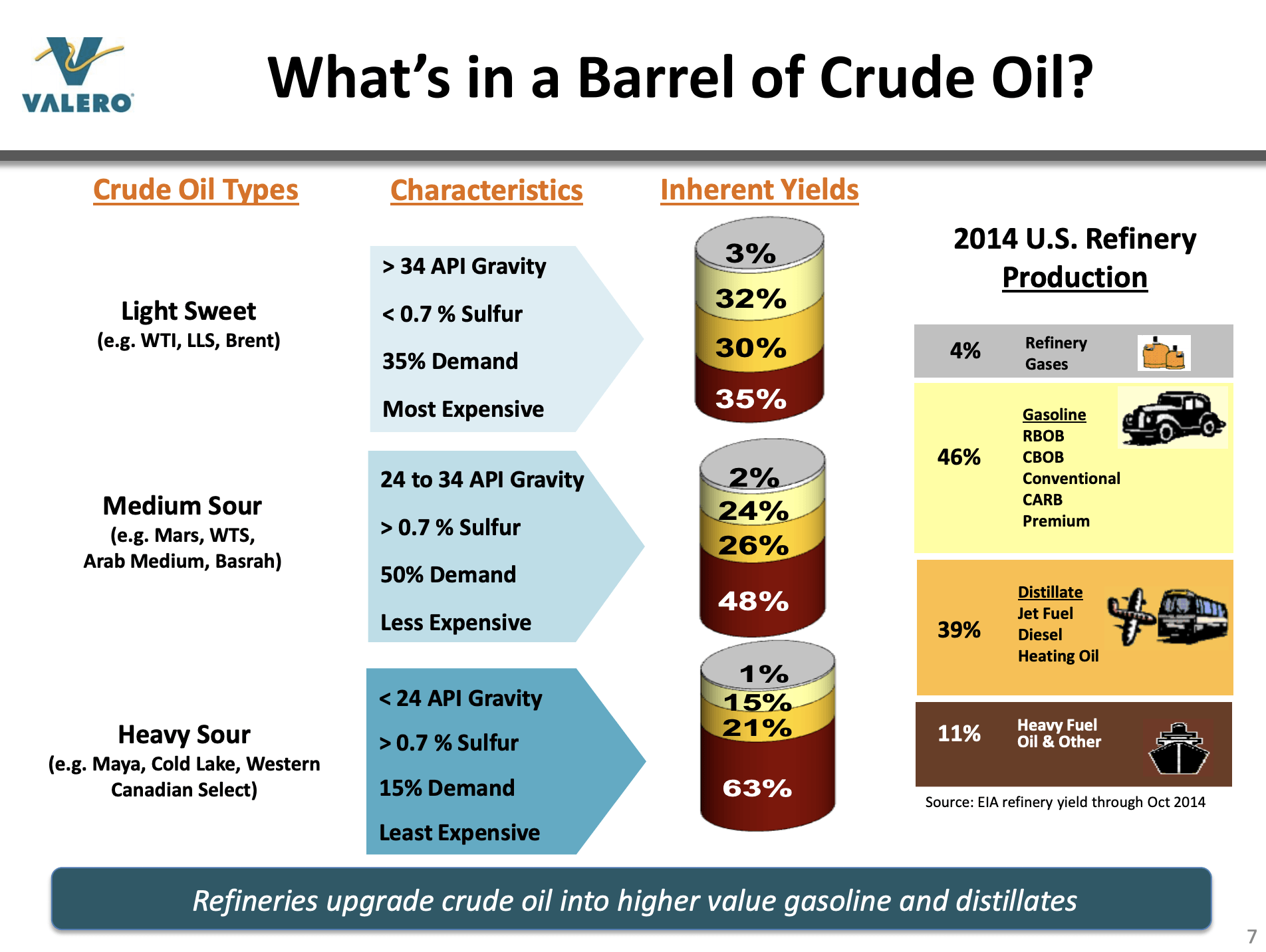

This step is called capacity rationalization. In essence, it's similar to what we see on the producer side. Simple refineries that can't control the type of products they produce and are at the whims of massive fluctuations in margins will be the first to shut down. A good example of this is a complex refinery in Asia that's able to process heavier crude (cheaper input cost) while producing more profitable products like distillate and jet fuel (not during COVID-19, but during normal times). While a simple refinery will be subjected to the normal processing limitations of each crude blend they buy. See this great explanation here.

Source: VLO

Another way to think about this is that a simple refinery is a high-cost producer of refining products, and complex refineries are lower-cost producers.