Summary

- Baker Hughes continues to expect a 50% fall in drilling and completion activity in North America in 2020 following the pandemic, which will adversely affect its short-term performance.

- Its management has become more pessimistic about the revival of the international energy market, although some geographies are still economically viable.

- The company, however, continues to move towards natural gas, NGL, and clean energy-related business transformation.

- BKR's balance sheet is more robust than many of its peers, while cash flows improved in Q2.

Baker Hughes Stays Put For A Medium-Term Revival

In the medium-to-long-term, Baker Hughes (BKR) looks to establish itself as a leading service provider in the natural gas and NGL-related business and clean energy industry. But, it has to overcome a few hurdles to reach there. As of now, the international offshore recovery has turned out to be elusive in the short term, although some still offer green shoots in the near term. The U.S. completions activity will stay muted in the next few quarters, as earlier expected. So, the company will look to add to its higher-margin products in the Digital Solutions segment. The $700 million cost reduction target is afoot, but its bottom-line will shrink from the remaining restructuring-related expenses in 2020.

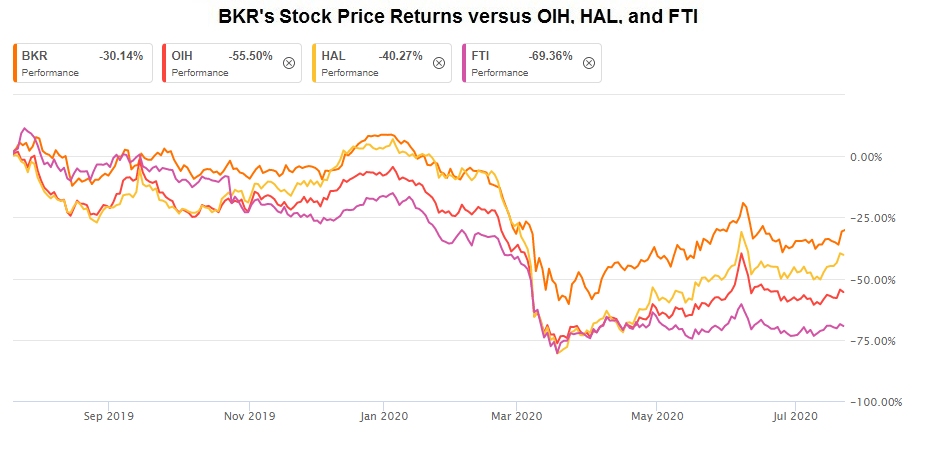

In Q2, the company's oilfield equipment backlog increased substantially, which can mitigate an otherwise falling revenue and margin potential in the next couple of quarters. I think BKR's stock price will stay depressed in the short term. However, the opportunities in the natural gas business, a robust balance sheet, and improved cash flows should provide upside in the medium-to-long-term.