Summary

- Q1 results show the impact of COVID-19 crisis.

- Liquidity and minimal leverage are assets in the current downturn.

- The robust dividend yield compensates the patient investor.

Because its fiscal year ends in February, Ennis Inc. (EBF) was one of the first companies to report quarterly results that fall entirely within the time of the COVID-19 pandemic. Before the market opened on June 22nd, Ennis reported first quarter results for the three months ended May 31.

As expected, revenue and profitability were sharply down in the current economic environment. However, the company's liquidity position and cash flow generation should allow it to survive an extended economic slowdown, and to thrive in a recovery scenario. The current share price and robust dividend yield offer investors an enticing entry point.

Q121 Results

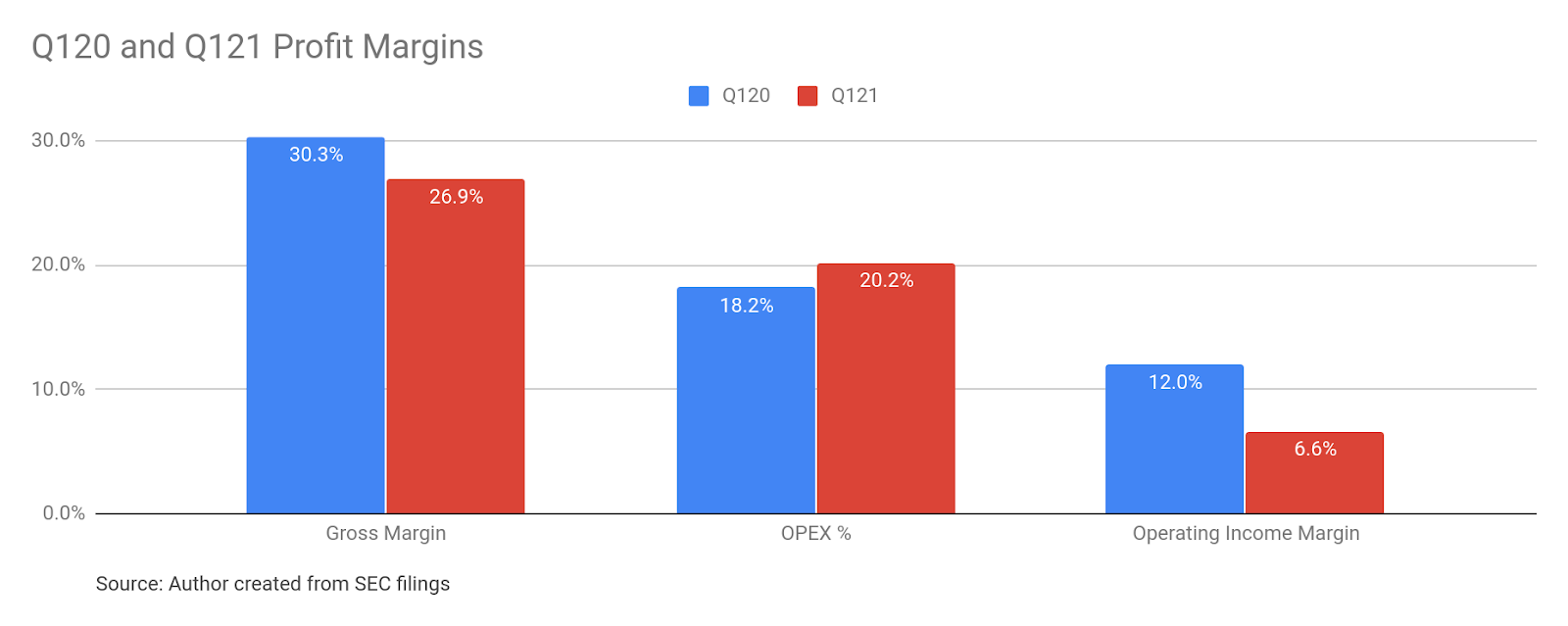

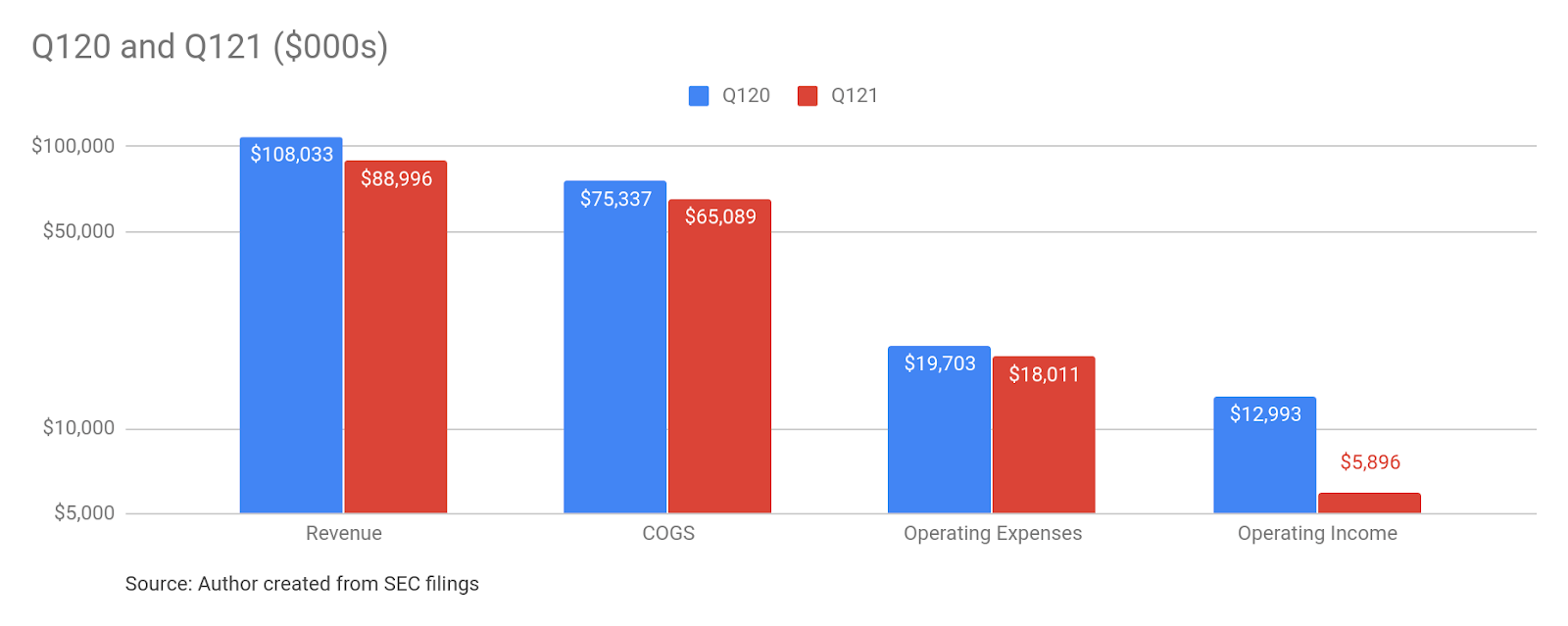

First, the bad news. Ennis saw its revenues in the quarter drop by $19.0M, or 17.6% from the prior year. Sequentially, the decline in revenues was 16.6%. To make matters worse, the cost of goods sold fell by a lesser amount in the quarter, leaving gross margin at just 26.9%, compared to 30.3% in the prior year quarter.

On top of this, operating expenses also declined by a smaller percentage than revenues. For the quarter, operating expenses as a % of revenues increased by 200 basis points to 20.2% from 18.2% for the prior year quarter.

The combination of the sharp drop in revenues, 340 basis point decrease in gross margin, and relatively minor 8.6% drop in operating expenses resulted in operating income for the quarter of just $5.9M, or 54.6% less than the $13.0M in the prior year quarter.

Not surprisingly, earnings followed suit. EPS for the quarter was $0.16, which is 56.8% less than the $0.37 EPS for Q120. What is surprising is that Ennis' shares rose about 5.8% on June 22 after the results were announced.

Market Reaction

So why would such a poor showing translate into investor enthusiasm? The broad market averages were essentially flat on the day (SPY was up 0.6%, DIA was up 0.6%, and VTI was up 0.7%) so we can discount a 'piggyback' effect.

The reason for the immediate pop in Ennis' shares was likely the fact that the poor results were better than analysts' estimates. Specifically, EPS at $0.16 was significantly better than the $0.12 projected for the quarter, while revenue at $89.0M was also better than the estimate of $88.2M.

Another factor driving the shares was that operating cash flow ('OCF') declined during the quarter by only 5.2%, despite the massive drop in profitability. Ennis was able to limit its OCF decline by maintaining a stable level of inventory while it used only a portion of the cash it received from the collection of accounts receivable to pay down its payables and accruals.