Summary

- Six Flags has suffered unevenly due to the pandemic.

- The stock has now moved close to our fair value prior to the pandemic.

- The market's optimism is misplaced.

- I do much more than just articles at High Dividend Opportunities: Members get access to model portfolios, regular updates, a chat room, and more. Get started today »

This article was highlighted for PRO subscribers, Seeking Alpha's service for professional investors. Find out how you can get the best content on Seeking Alpha here.

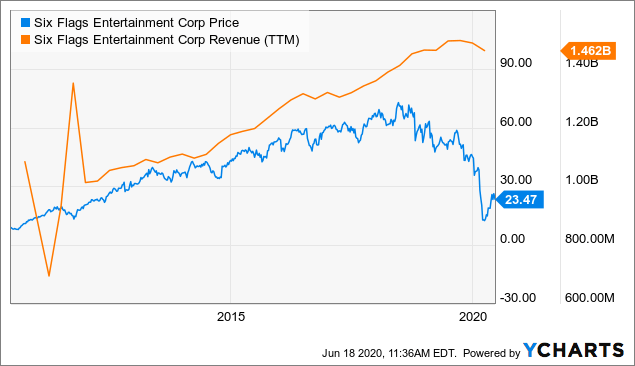

Prior to the pandemic we felt Six Flags Entertainment Corporation (SIX) would offer some value near the $25 mark. Specifically we said,

On the other hand, the franchise is not going anywhere and in this market we can see value for the shares if they hit the $24-$26 price range. Even the most ardent bulls should pause and calculate what these adjusted EBITDA numbers would look like in a recession before taking the plunge. Cash secured puts still remain far more attractive than the common shares and one could argue that the dividend cut has made them even more attractive versus the common. Anyone bullish on the shares should simply sell the $30 or $25 puts to establish a position and let the shares come to your buy point.

Source: Six (Red) Flags: Free Cash Flow Profile Dictated The Large Cut

Of course all sanity went out of the market as investors fled the hardest hit sectors. SIX initially crashed to the $8 dollar range but since then has bounced right back to what we considered a decent price if everything was normal. Considering everything is not remotely normal, we decided to see if this would make a compelling short.

The Current Situation

The Company has almost completely suspended its operations in all theme parks. It has introduced guest reservation systems for the future and plans to enable guests to maintain high levels of social distancing when it opens. With the summer of 2020 being more or less a complete write off, attention has turned to the future years to get a sense of valuation. This is where the rubber meets the road.

Debt

At first glance, the debt situation looks manageable. Net debt as of March 31, 2020 was $2,241 million representing a net leverage ratio of 4.3 times adjusted EBITDA. The Company had total liquidity of $832 million at the end of Q1-2020 and no debt maturities until 2024. The debt though will go up as SIX will burn through $30-$35 million each month the parks remain closed. More importantly, investors need to ask what the company will look like on the other side.

A Baseline Number

SIX was going through some problems even before the pandemic and its debt to EBITDA was expected to climb markedly. We were expecting a baseline 2020 number of 4.7X. Of course those numbers are going to be nowhere in sight. But let's look at 2021 and see where we go with the debt to EBITDA. Starting off with the $2.24 billion in debt and adding a good $270 million till end of the year, we come to starting point of $2.5 billion.What kind of revenues can the company generate in this environment? Over the past few years SIX has generated increasing revenues through significant capex.

Data by YCharts

Data by YChartsConsidering even a modestly quick recovery, it seems highly probable that the employment situation will remain weak well into 2021 or 2022. It would be hard for the company to generate anywhere close to 2016 or 2017 revenues in that case, but assuming it gets there, we are still looking at $1.2-$1.3 billion in revenues alongside $300-$350 million in adjusted EBITDA. Debt to EBITDA in that case leads to blowout of over 8X at the low end.