Summary

- Falling oil prices have punished names like BKR. My sell thesis has played out.

- BKR trades at less than 6x EBITDA. I believe the bad news is priced in.

- Oil supply cuts will help oil prices. People will also return to work, improving demand for oil.

- BKR appears poised to benefit from any upside in oil prices. The sell thesis is over. Buy the stock.

- This idea was discussed in more depth with members of my private investing community, Shocking The Street. Get started today »

Baker Hughes CEO Lorenzo Simonelli. Source: Houston Chronicle

Baker Hughes CEO Lorenzo Simonelli. Source: Houston Chronicle

The global economy has been brought to a standstill to help stem the spread of the coronavirus. A recession is likely upon us. It may be a matter of how long it will last. Less talked about is the sharp fall in oil prices. Brent oil is sub-$30, and it has weighed on oil-related names like Baker Hughes (NYSE:BKR). The stock is off over 45% Y/Y. The decline likely reflects the free fall in demand for oil, but that could change.

More Stagnation In North America?

Oil prices have received the benefit of OPEC supply cuts for years. I have wondered aloud if demand for oil justified robust E&P in the oil patch. The coronavirus has led to social distancing and a free fall in demand. After President Trump's urging, Saudi Arabia and Russia agreed to a production cut. After the pandemic ends, demand for oil should rise, driving prices and E&P higher. This should benefit Baker Hughes.

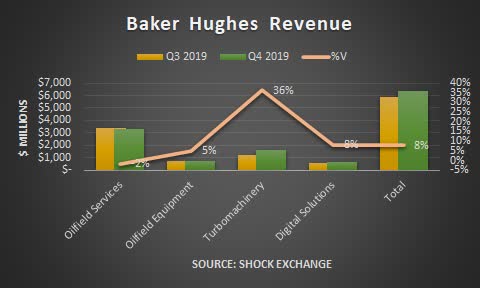

In its most-recent quarter, Baker Hughes reported revenue of $6.3 billion, up 1% Y/Y and 8% sequentially. This followed a 3% sequential decline in Q3. Along with Schlumberger (SLB) and Halliburton (HAL), Baker Hughes is one of the largest players in the North America land drilling market. This segment has faced headwinds due to budget exhaustion experienced by certain clients. In Q4, Halliburton and Schlumberger both experienced double-digit revenue declines in North America.

The company's short cycle businesses included Oilfield Services and Digital Solutions. Baker Hughes generated a combined $4.0 billion in revenue from these businesses, flat sequentially and up 5% Y/Y. They represented 62% of the company's total revenue, so their performance still has a sizeable impact on Baker Hughes's operations. The U.S. rig count was stagnant to declining for most of 2019. It fell by double digits in Q4 2019. For the week-ended April 17th, the U.S. rig count fell by 73. This suggests E&P in the oil patch could face more headwinds.

The company's short cycle businesses included Oilfield Services and Digital Solutions. Baker Hughes generated a combined $4.0 billion in revenue from these businesses, flat sequentially and up 5% Y/Y. They represented 62% of the company's total revenue, so their performance still has a sizeable impact on Baker Hughes's operations. The U.S. rig count was stagnant to declining for most of 2019. It fell by double digits in Q4 2019. For the week-ended April 17th, the U.S. rig count fell by 73. This suggests E&P in the oil patch could face more headwinds.