While sluggish commercial real estate investment activity has caused loan closings to slow in Q3 2020, a rise in loan applications in recent weeks is a promising sign for higher year-end closings, according to the latest research from CBRE.

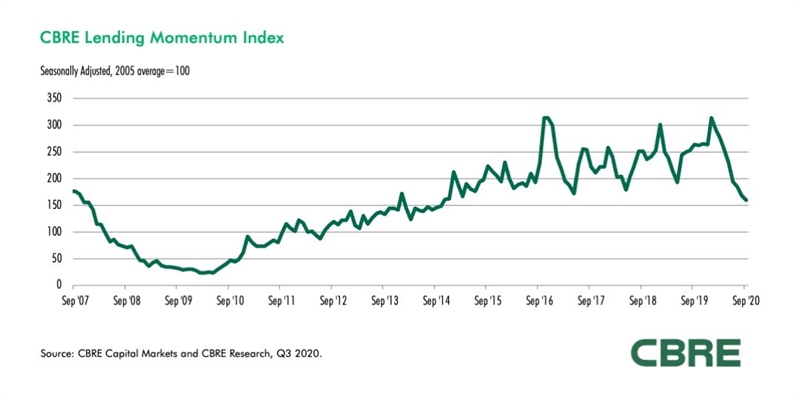

The CBRE Lending Momentum Index, which tracks the pace of commercial loan closings in the U.S., fell to a value of 160 in September, down 17.6% from June. As of September 2020, the index was down 39.4% from a year ago.

“Stabilized multifamily continues to receive strong support from the agencies, while banks and life companies continue to underwrite lower leverage multifamily, industrial and selective office transactions. Retail and hotel properties, as well as those properties with transitional issues, remain challenging to underwrite. One promising sign has been the re-emergence of quotes from alternative lenders in recent weeks, a source of capital for value-add properties and distressed situations,” said Brian Stoffers, Global President of Debt & Structured Finance for Capital Markets at CBRE.

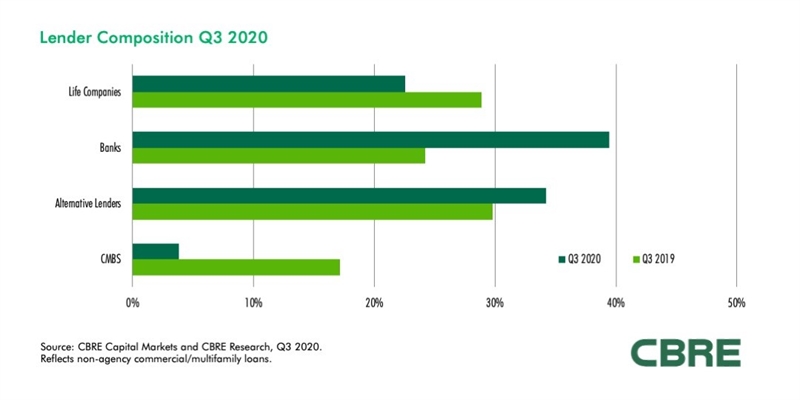

CBRE’s lender survey indicates that banks relinquished market share to other lenders in Q3 2020 after capturing over 70% of loan originations in the previous quarter. Banks still led the major non-agency lending groups by capturing 39% of loan closings in Q3 2020. Banks funded mostly five-to seven-year permanent loans concentrated in the multifamily and industrial sectors, with a few select office and retail deals. Bank lending has primarily been focused on smaller, local and regional banks and credit unions—as many of the large money-center banks continue to assess their existing portfolios.

Alternative lenders (includes REITs, finance companies, debt funds), which did little lending in Q2 2020, accounted for 34% of loan volume in Q3 2020. These lenders closed a variety of multifamily and retail bridge and construction deals during Q3 2020.

Life companies accounted for 22.5% of non-agency loan closings in Q3 2020, consistent with recent quarters and largely low-leverage at approximately 50% average loan-to-value (LTV). The majority of these loans were for office, multifamily and single-tenant retail assets.

Reflecting the disruption to public capital markets earlier in the year, CMBS closings were thin in Q3 2020. Industry-wide CMBS issuance was $10.4 billion in Q3 2020, bringing the year-to-date total to $40.4 billion compared with $58.7 billion for the same period last year.

Loan underwriting measures turned more conservative for the second consecutive quarter. The average debt service coverage ratio (DSCR) was 1.59 in Q3 2020, up from 1.38 a year ago. The average LTV was 61.5%, down from 67.2% in Q3 2019.

“Loan underwriting has become more conservative in the current risk-adverse lending environment. Average LTVs for permanent commercial and multifamily loans fell in Q3 to levels not seen since the Global Financial Crisis,” added Mr. Stoffers.

About CBRE Group, Inc.

CBRE Group, Inc. (NYSE:CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm (based on 2019 revenue). The company has more than 100,000 employees (excluding affiliates) and serves real estate investors and occupiers through more than 530 offices (excluding affiliates) worldwide. CBRE offers a broad range of integrated services, including facilities, transaction and project management; property management; investment management; appraisal and valuation; property leasing; strategic consulting; property sales; mortgage services and development services. Please visit our website at www.cbre.com.