Summary

- The valuation of Sinclair against peers makes the company highly attractive.

- Though problematic, the value the market is placing on the RSNs is now below what they may actually be worth.

- Technically, the selling may be exhausted.

Before getting into the specifics of this article, I want to make it clear that despite tagging my previous coverage of Sinclair (SBGI) as Bullish, I very openly stated that it was possible the stock could trade below $30 again. In fact, the title of the article was "Buying Short Term Weakness in Sinclair Will Pay Off Next Year." And here we are. We've had plenty of weakness and it's 2020. And since my main reasons for buying centered around revenue injections from political and the Super Bowl, we've yet to see that theory disproved. So, just what the heck has happened since that published piece? Confidence has been decimated and I totally understand why. EPS missed expectations, profits disappointed, and the Q4 conference call was... not great. All of those things are good reasons to sell the stock. But as we'll explore in this article, I believe Sinclair is a buy at this price.

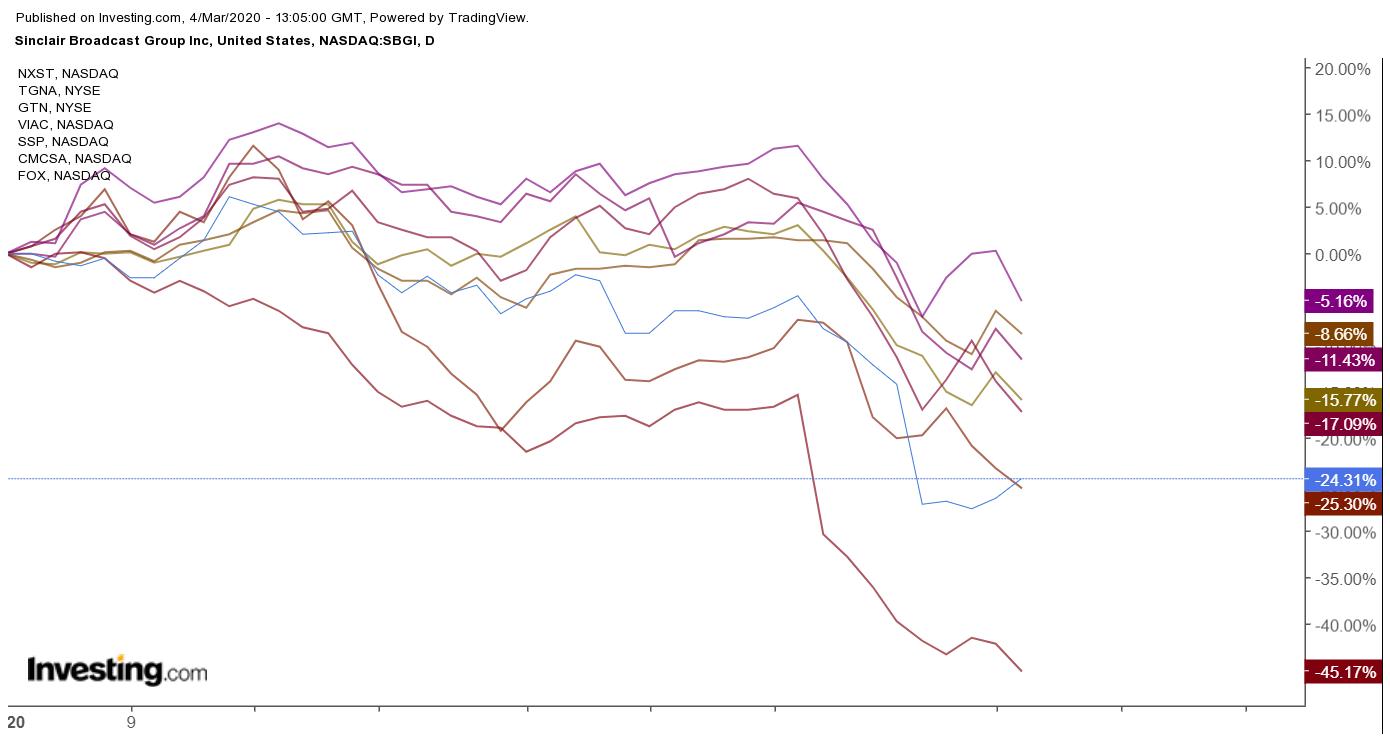

Broadcast has been crushed hard YTD

Though the selloff in Sinclair over the last eight months has been vigorous, the sector is seeing weakness in a lot of names. Though it has lagged most of those peers year to date, Sinclair's performance has been about even with Scripps (SSP) and much better than that of ViacomCBS (VIAC). Considering what the broad market has gone through in the last two weeks, you could argue Sinclair has held up fairly well the last few sessions. Of the names in the space, SBGI (blue line) appears to be the only one to have established anything resembling a bottom.

(Source: Investing.com)

In the past, I've liked to look at metrics like price-to-book, sales, and yield. Based off those metrics, Sinclair is the cheapest of the local broadcast bunch.

{kind=link}