Summary

- Sonoco Products provided 2020 guidance on December 6th. The market gave it little more than a token nod.

- A giant in the packaging industry, Sonoco expects growth in revenue, cash flows and base earnings in 2020. Based on Sonoco's averages for typical metrics, the stock appears slightly undervalued.

- Yet, typical metrics short-change the potential of Sonoco, its focus on a bigger picture and its role in marrying sustainability with solutions addressing the food waste crisis.

Sonoco Products (SON) provided 2020 guidance on December 6th, and the market gave it little more than a token nod. The share price finished the day approximately 2% higher than its open. It has since given up approximately half of that gain.

Either the guidance was uninspiring or the news already priced in. Since the shares are still trading approximately 10% off the 52-week high, it would seem guidance was uninspiring. And, yet, in my opinion, that's simply not the case.

Sonoco's 2019

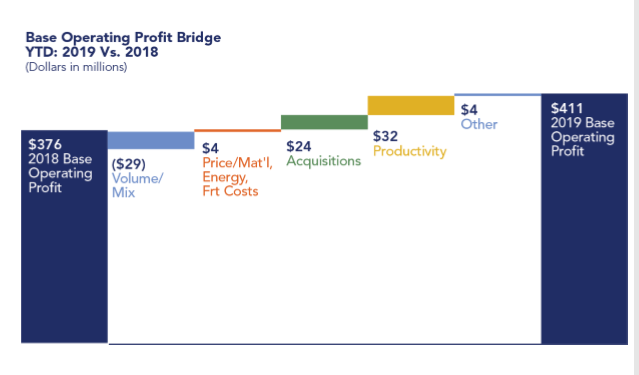

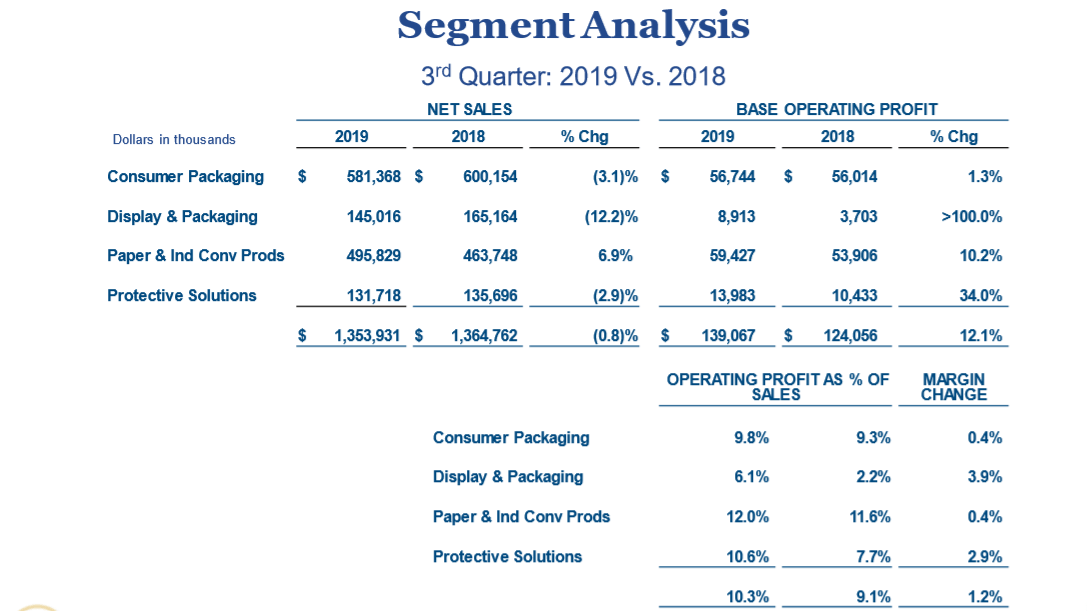

When the global diversified packaging provider to both consumers and industrial businesses reported its 2019 third-quarter results on October 17th, net sales year-to-date had tallied a slight improvement from $4.04 billion in 2018 to $4.07 billion. The bottom line through the first three quarters had improved 4.3% from $2.34 in 2018 to $2.44 per diluted share.

"Results in the first nine months of the year benefited from earnings from acquisitions, productivity improvements, cost controls and a slightly positive price/cost relationship which more than offset lower volume mix and the negative impact of foreign exchange."

Sonoco's focus on improving productivity and controlling costs had the greatest impact on operating profit.

"By focusing our business on the areas which we can control, we continue to drive margin expansion as each of our four business segments report gains in operating profit as compared to last year."

Regarding the top line, Sonoco pointed to the global slowdown as having the greatest impact.

"Our customers are tightening inventories and closely watching new orders with expectations for slower demand."

For the full year, Sonoco expects base earnings per share in a range of $3.50 to $3.54. Base earnings are Sonoco's non-GAAP comparative measure defined as earnings excluding restructuring-related items, asset impairment charges, acquisition expenses, non-operating pension costs, and certain other items. In 2018, base earnings totaled $3.37 per share. Thus the year-over-year improvement equates to approximately 4.5%.

With just a few weeks remaining in the final quarter of 2019, the company also reaffirmed guidance for operating cash flow and free cash flow. Operating cash flow for the first three quarters totals $239 million and is expected to fall in a range of $435 million to $455 million. Free cash flow for the first three quarters is actually negative, but is expected to fall in a range of $60 million to $80 million for the whole year. The cash flow projections include an impact from Sonoco's voluntary contribution to its pension plan of $200 million.

Operating cash flow and free cash flow in 2018 were $590 million and $260 million, respectively. Thus, it would seem the totals in 2019 are a disappointment. But, in actuality, the original estimate for operating cash flow was a range of $600 million to $620 million and for free cash flow was a range of $225 million to $245 million. The voluntary pension contribution in the second quarter had an after-tax impact of $165 million.