Summary

- We gave our most important investing advice a few months ago and recommended AT&T as a must-own.

- A huge rally in the stock is justified as we go behind the idea to look at performance metrics and future outlook.

- We expect EPS growth to be about $3.75 in 2020 and approach $4.50 by 2022.

- A safe dividend still yielding well over 5% cannot be ignored.

- Looking for a helping hand in the market? Members of BAD BEAT Investing get exclusive ideas and guidance to navigate any climate. Get started today »

At the time of this writing, AT&T (T) is trading higher following its highly anticipated Q3 earnings report. This report comes after we highlighted the stock as the most important investing advice we could give. The stock has rallied hard in the last few months, and we believe today's report and outlook justify the rally. The company is evolving. Major milestones such as the closing of the Time Warner deal are done. The company has started to really recognize its debt burden and begun to offload assets left and right, something we see as vital to the stock's success. All the while it has continued to compete as a global telecommunications giant known for its healthy dividend yield. It's a fantastic income name and, in our opinion, also serves as a wonderful name to compound in a tax-favored account for decades. In this article, we go a bit more behind the idea of owning this name and look to underlying performance. We are continued buyers because of strong performance. There are key strengths and weaknesses to be aware of, but, ultimately, we see earnings continuing to ramp up into the next decade.

Top-line pressure remains

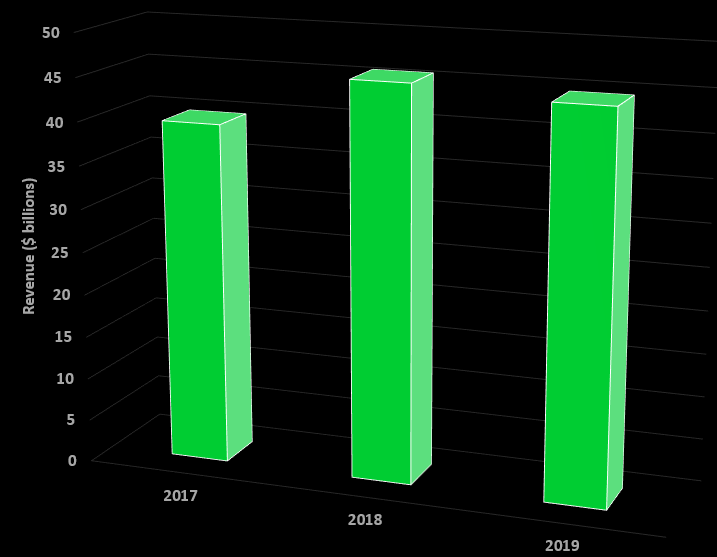

Revenues had begun to flatten for the company in recent quarters until Time Warner's assets were brought under the AT&T umbrella. We are seeing the positive impact, but revenues in Q3 showed slight contraction from a year ago:

Source: SEC Filings, graphics by BAD BEAT Investing

All in all, our revenue expectations were slightly more liberal relative to the pack. Analysts covering the company were targeting a consensus of $45.07 billion. We were targeting $45.10 billion for this metric as we felt the impacts from the loss of video subscribers from struggling DirecTV and ongoing promotions in the wireless business would continue to show some resolve following a heavy quarter for pushing to get new customers. However, the posted result of $44.58 billion was well below estimates

So, what drove the top line? Well, declines in revenues from legacy wireline services, WarnerMedia, and domestic video were partially offset by growth in strategic and managed business services, domestic wireless services, and IP broadband. As the race to consolidate services continues, many are disconnecting from such services, including opting for AT&T owned HBO NOW. We had anticipated ongoing promos. The hit in video entertainment subscribers was higher than anticipated. In fact, AT&T lost 1,163,000 TV subs and lost 195,000 AT&T Now subs. That said, the group as a whole saw operating income and EBITDA growth. So, despite the subs number, performance was up.