Summary

- Marriott Vacations guidance largely confirmed Street views on its growth, margins, and FCF.

- $1.3-2.3 billion of cash generated through 2022 should create significant shareholder value.

- Multiple growth levers exist for VAC, including digital initiatives and driving sales at ILG.

- Its points-based timeshare model should prove resilient in mild economic downturns.

- VAC shares are trading at 7.5x 2021 EBITDA vs. HGV at 9x.

Marriott Vacations Worldwide Corporation (VAC) recently hosted its 2019 Investor Day, where it notably guided to a financial plan through 2022 that confirmed Street expectations for revenue, contract sales, and adjusted EBITDA growth. Management expects $1.3-1.5 billion of FCF to be generated through 2022, which is earmarked for strategic M&A or shareholder return via dividends and share repurchases. Further, annual synergies from the integration of ILG have proven to be greater than expected ($125+ million versus the previously expected $100+ million).

Despite this mostly in-line guidance, VAC's confirmation of Street expectations leaves me more upbeat about its pressured valuation context. In my view, VAC offers fantastic value for investors given the multiple organic levers for growth that it presents, its seemingly resilient business model regardless of its discretionary nature, and its strong capital return plans.

I suspect investors have been wary of VAC owing to its sensitivity to the macroeconomic environment. However, I would emphasize the progress VAC has made to a points-based timeshare system (from a weeks-based one), which is more resilient to economic downturns.

I believe a near-term catalyst to generate value for the stock could be further news on Hilton Grand Vacations Inc (HGV) buyout, as reported earlier by the New York Post.

Multiple Levers for Growth and Efficiency

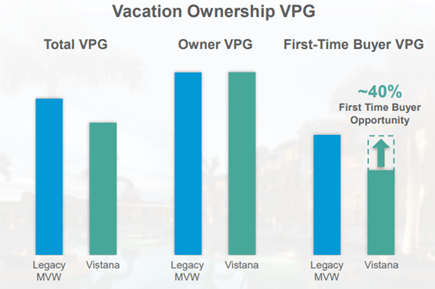

VAC underlined select growth levers this Investor Day that added to my confidence in its growth prospects; a key initiative that should seemingly drive organic growth for VAC is its digital marketing initiatives to offset declining volumes of its Call Transfer initiatives. Presently, digital is only ~2.5% of VAC's mix, which provides significant room to grow its digital channel and reach a greater audience. Meanwhile, management also intends to help Vistana close the 40% first-time buyer VPG (a measure of sales effectiveness) gap versus legacy Marriott Vacations by importing VAC's 'principles of direct sales excellence' to ILG (see Exhibit 1). Irrespective of the macroeconomic environment, such initiatives should help VAC continue to grow revenues year-over-year, given that they rely on tapping into existing inefficiencies at the company.

Exhibit 1

Source: Marriott Vacations Worldwide