Summary

- Altria got a bit of good news on Friday, with Bank of America Merrill Lynch reiterating its buy rating on the stock.

- At the same time though, the credit default swaps market was signaling a warning flag for Altria: a 6% chance of default over the next 5 years.

- That chance of default had climbed from 4% last Monday.

- For cautious bulls looking to limit their downside risk in light of that, I show ways of doing so while staying long.

- Looking for a helping hand in the market? Members of Bulletproof Investing get exclusive ideas and guidance to navigate any climate. Get started today »

A 1953 ad in the Saturday Evening Post for Altria's Philip Morris brand (photo via Pinterest).

Good News And Bad News For Altria

Seeking Alpha News Editor Clark Schultz noted a bit of good news for Altria (MO) on Friday ("Altria in the spotlight"): Bank of America's (BAC) Merrill Lynch unit reiterated its buy rating on the stock, which is trading at its lowest earnings multiple in 10 years. That buy rating is consistent with the average rating of Seeking Alpha contributors on the stock.

Screen capture via Seeking Alpha

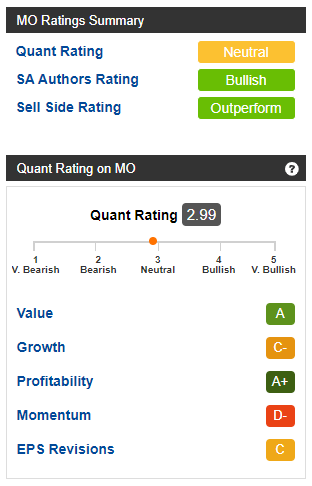

Given the value tilt of many Seeking Alpha contributors, their current bullish rating is understandable. In contrast, Seeking Alpha Essential's Quant Rating, which takes into account momentum in addition to value and three other sub-components, was neutral on the stock.

Although Merrill Lynch's reiterated buy rating was good news for Altria shareholders, there was a bit of bad news regarding spreads on the company's senior 5-year default swaps, as Bloomberg's Brian Chappatta tweeted last Monday.