Summary

- Altria and Philip Morris have been battered recently by news that they are considering merging, creating a lot of uncertainty and dividend safety angst.

- A $200 billion merger of equals makes great strategic sense, and would create a stronger company that would likely keep growing at 8% or so, for many years to come.

- The potential downsides and risk of a potential stealth dividend cut (for MO shareholders) isn't enough to scare me away from buying or recommending either stock today.

- The final decision on the merger is likely to come within a month or two, and possibly serve as a strong short-term positive catalyst for both companies.

- Today PM and MO are 17% and 30% undervalued, respectively, and offering 13% to 20% and 15% to 23% CAGR respective long-term return potential.

- I do much more than just articles at The Dividend Kings: Members get access to model portfolios, regular updates, a chat room, and more. Get started today »

(Source: Imgflip)

(Source: Imgflip)

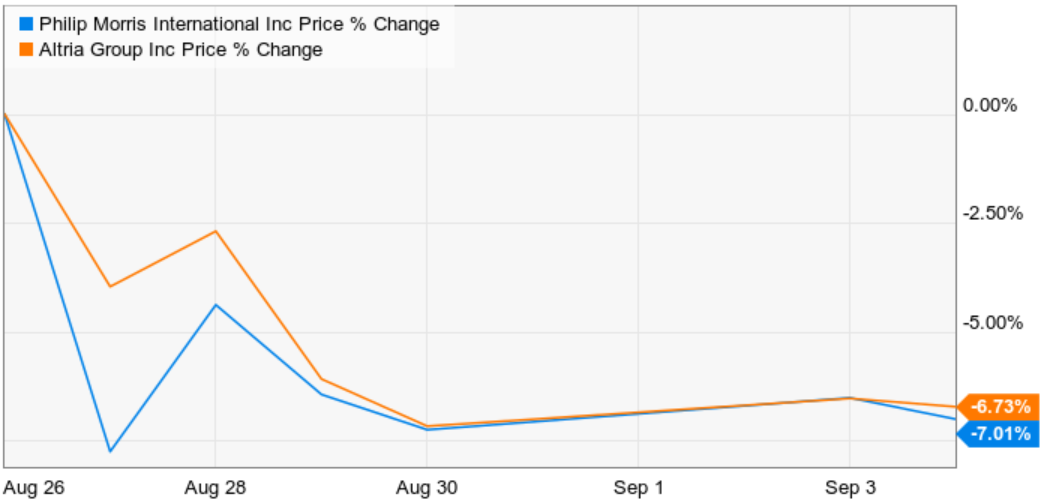

It's been a rough two years for tobacco stocks in general, and not even legendary dividend kings like Altria (MO) or Philip Morris International (PM) have been spared.

On August 27th, both companies confirmed they are discussing a possible $200 billion all-stock merger of equals, which the market has reacted badly too.

(Source: Ycharts)

That has caused both stocks to languish in their respective severe bear markets, now down more than 40% off their 2017 all-time highs (when both were overvalued).