Summary

- Improvement in order intake in Turbomachinery & Process Solutions and Oilfield Services segments in Q2.

- Steady growth in LNG production in the medium-to-long term should drive growth, while the Subsea Connect and flexible pipe business give BHGE a competitive advantage.

- Falling order in the Oilfield Equipment points to a challenging industry environment.

- Negative free cash flow in 1H 2019 is a concern.

- Looking for more stock ideas like this one? Get them exclusively at The Daily Drilling Report. Get started today »

Baker Hughes May Start Improving In The Medium Term

Baker Hughes, a GE Company (BHGE) is a fullstream oilfield technology provider which offers integrated equipment and service capabilities. GE owns ~62.5% of the combined company’s shares. I think BHGE’s stock price is due for a rebound in the medium-to-long term unless the industry faces another ugly downturn. In the short term, the stock is likely to remain range-bound, but a steady Q3 should keep it from deteriorating further.

In recent times, the healthy order intake in Turbomachinery & Process Solutions and Oilfield Services segments has improved revenue visibility. The company has received several significant projects in the Middle East and the North Sea. Also, the increased activity in other geographies is expected to benefit the company in the medium term. The steady growth in LNG production should complement the company’s Subsea Connect suite of products and technology and give it an advantage in a competitive industry.

On the other hand, the two primary concerns for BHGE are the falling Oilfield Equipment segment backlog and negative free cash flow. Over the medium term, debt repayment can become difficult unless the company improves its free cash flow or refinances the debt.

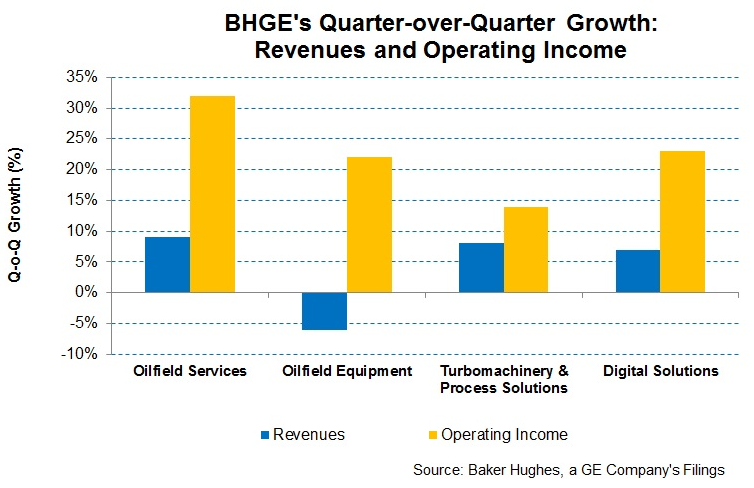

Analyzing The Oilfield Services Segment

Baker Hughes’ Oilfield Services segment recorded the highest revenue and operating income growth among its segments in Q2 2019 compared to a quarter ago. Quarter-over-quarter, while its revenues increased by 9%, operating income inflated by 32%. Recovery in the E&P activity in international markets primarily led to the growth following the ramp-up of the integrated well services contracts. On top of that, higher cost absorption in Q2 caused the operating margin to improve.

In the flexible pipe business, order activity is likely to improve in 2H 2019 compared to a year ago. The oilfield services market is typically a short-cycle market. So, BHGE’s growth in the U.S. is likely to remain subdued in the short term. The international market, led by the activity spurt in the Middle East and the North Sea, is expected to witness growth as other regions like Sub-Saharan Africa, Asia-Pacific and Latin America join the upside in the medium term.