Summary

- As I suggested in my last Seeking Alpha article on Phillips 66, the company's awful Q1 was an aberration and a "one-off".

- That turned out to be the case. Q2 was more like what we have come to expect from Phillips 66: $3.12 in quarterly EPS and a 12.5% dividend boost.

- Going forward, Phillips 66 has the growth projects to continue to grow the dividend and deliver excellent total returns.

- Meantime, eliminating the IDRs and GP interest at its MLP will grow PSX's LP ownership level in it to 75%.

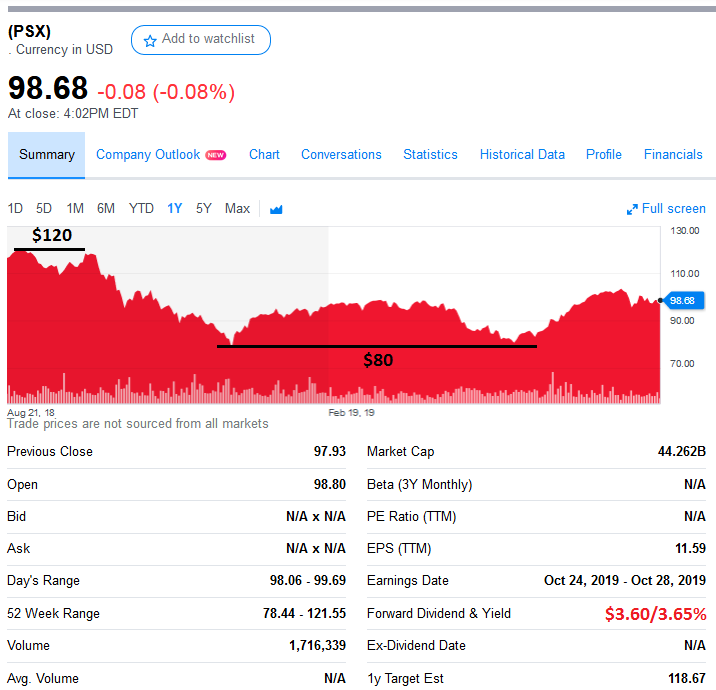

Phillips 66 (PSX) has been a quite a ride over the past year, trading from $120 to below $80. Everything from Buffett and Berkshire (NYSE:BRK.A) (NYSE:BRK.B) selling to an awful Q1 EPS report has rocked the shares. The stock now sits in the middle of that range. As I mentioned in my last Seeking Alpha article on PSX (See: Phillips 66: Serious Cash Flow Generation Despite Q1 Aberration), the Q1 EPS report was an anomaly and "one-off" for fairly obvious reasons. I've been following PSX since the spin-off, and have never seen Phillips 66 report a quarter similar to Q1 before.

Source: Yahoo Finance (price lines and dividend info added by the author)

Source: Yahoo Finance (price lines and dividend info added by the author)

The Q2 Earnings Report

And the Q2 EPS report proved me exactly right. The Q2 report was excellent and more of what shareholders have come to expect from the company:

- Earnings of $1.4 billion or $3.12/share.

- Generated $1.9 billion in operating cash flow; returned $861 million to shareholders.

- Increased quarterly dividend by 12.5% to $0.90 per common share.

- Operated at 97% utilization in Refining.

- Delivered record Midstream results.

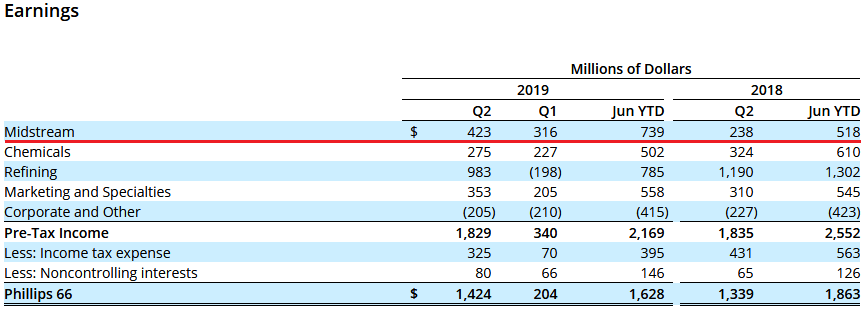

The graphic below shows strong financial results across all segments, with the Midstream segment being particularly strong:

Source: Q2 EPS Report

Source: Q2 EPS Report

Midstream benefited from higher pipeline and terminal volumes at both wholly owned and joint venture operations, higher margins and volumes at the Sweeny Hub, improved butane trading results, and higher distributions from DCP Midstream (DCP) - primarily reflecting favorable hedging impacts. DCP is a publicly traded MLP whose GP is 50% owned by PSX, and 50% owned by Enbridge (ENB). DCP owns 59 gas processing plants, 12 fractionators, and is one of the biggest producers of NGLs in North America.

The Marketing & Specialties segment ("M&S") also had a stellar quarter on the back of strong global margins and refined product exports of 187,000 bpd.