Summary

- One of the reasons AT&T's stock price is down is because of a fear in the marketplace that the company is carrying too much debt.

- AT&T has free cash flow available after paying its dividend to reduce its debt.

- The company has an aggressive strategy to reduce its net debt by $20 billion in 2019.

AT&T (T) saw its share price slide in the first half of 2018 as analysts poured over its potential takeover of Time Warner. Many analysts were concerned the company was taking on too much debt to complete its acquisition of Time Warner. The company has started executing on joining forces with Time Warner and the stock price has started to regain its footing. It is becoming apparent that analyst and investor fears that the company was taking on too much debt have been overblown.

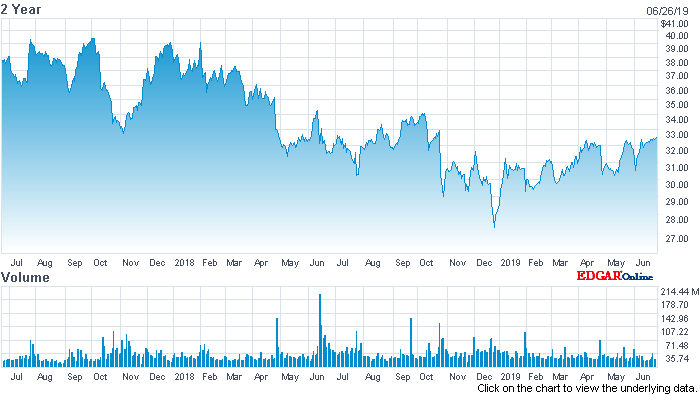

First let's take a look at the two year chart of AT&T's stock price over the last two years:

The stock price was consistently trading in the upper $30's prior to the announced acquisition of Time Warner. Since then it has consistently traded in the lower $30's. AT&T has a plan to lower its overall debt. Once Wall Street gets comfortable that the company does not have too much debt, then the stock price could start trading back into the upper $30's and maybe start trading over $40 per share. The company will need to execute on its debt reduction plan to regain Wall Street's confidence.

The stock price was consistently trading in the upper $30's prior to the announced acquisition of Time Warner. Since then it has consistently traded in the lower $30's. AT&T has a plan to lower its overall debt. Once Wall Street gets comfortable that the company does not have too much debt, then the stock price could start trading back into the upper $30's and maybe start trading over $40 per share. The company will need to execute on its debt reduction plan to regain Wall Street's confidence.

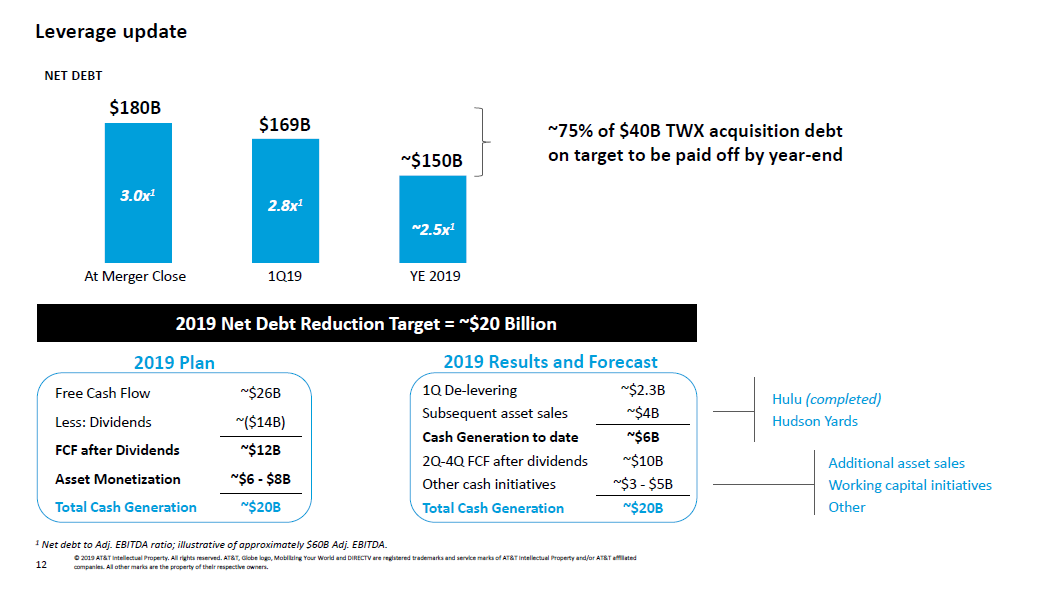

What is amazing about AT&T is the amount of free cash flow the company is generating. This despite spending aggressively to build out a nationwide 5G network for its mobile businesses. Here is a look at the company's debt reduction strategy for 2019:

AT&T had $180 billion in net debt after the Time Warner merger, and they plan to reduce that debt to $150 billion by the end of the year. The company is already making progress on that goal and has reduced its net debt to $169 billion by the end of the first quarter of 2019. As can be seen in the slide above, AT&T has tremendous free cash flow. Free cash flow should not be confused with concepts like Earnings Before Interest Taxes Depreciation and Amortization {EBITDA}. EBITDA is a cash flow concept about earnings before a company has paid any interest on its debt, paid any taxes, and it doesn't account for any capital expenditures needed to run the business. Free cash flow, on the other hand, is after a company has paid interest on its debt, paid any taxes owed, and made all of the capital expenditures necessary to run and invest in the business. It is money from operations left over and not needed to run the business.

AT&T had $180 billion in net debt after the Time Warner merger, and they plan to reduce that debt to $150 billion by the end of the year. The company is already making progress on that goal and has reduced its net debt to $169 billion by the end of the first quarter of 2019. As can be seen in the slide above, AT&T has tremendous free cash flow. Free cash flow should not be confused with concepts like Earnings Before Interest Taxes Depreciation and Amortization {EBITDA}. EBITDA is a cash flow concept about earnings before a company has paid any interest on its debt, paid any taxes, and it doesn't account for any capital expenditures needed to run the business. Free cash flow, on the other hand, is after a company has paid interest on its debt, paid any taxes owed, and made all of the capital expenditures necessary to run and invest in the business. It is money from operations left over and not needed to run the business.

The company is projecting free cash flow of $26 billion from operations in 2019. After choosing to pay $14 billion annually in dividends to shareholders, the company will still have $12 billion in free cash flow to reduce its debts. The company is also planning $6 billion to $8 billion in non-core assets sales, of which $4 billion worth have already been accomplished year to date. Right now there is every reason to believe AT&T will accomplish its goal of reducing its net debt to around $150 billion by the end of 2019. Then, the company anticipates generating more than $10 billion in free cash flow to reduce its debts further in 2020, and again in 2021, 2022, etc.