Summary

- Since the end of 2017, CNX Resources improved its leverage while growing its production and reducing its number of shares.

- Yet, the stock price dropped by more than 50% since last year.

- The attractive 17% free cash flow yield, corresponding to a flat production, is protected by hedges.

Over the last four quarters, the natural gas producer CNX Resources Corporation (CNX) grew its production, lowered its leverage, and reduced its number of shares outstanding. Also, management announced $500 million of free cash flow in 2020. At the current stock price, the corresponding 30%+ FCF yield is impressive.

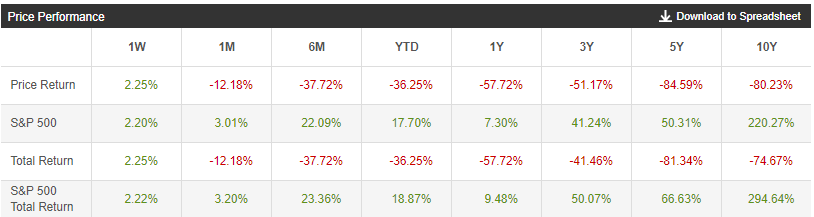

Yet, over any period of time you may want to consider, the stock price dropped and underperformed the S&P 500 by a wide margin.

Source: Seeking Alpha Essential

Many factors contributed to the stock price decline. For instance, the expected 2020 free cash flow isn't sustainable and is due to the timing of the capital program. Also, management increased the 2019 capital program and reduced EBITDAX guidance.

With Will Thorndike as chairman, I'm not concerned about capital allocation decisions. He's the author of the book "The Outsiders: Eight Unconventional CEOs and Their Radically Rational Blueprint for Success." In its latest letter to shareholders, he insisted on creating long-term value by increasing the NAV per share thanks to a focus on capital allocation decisions. It doesn't mean he will succeed. But he has at least the right mindset to create value for shareholders.

With this context, let's have a look at the recent results before assessing the free cash flow potential and the valuation.